Limited Liability Partnership

Sonam Geda & Company

Features of Limited Liability Partnership

- An LLP is a form of organization which is having combined features of a partnership as well as companies and it is registered under Limited Liability Partnership Act 2008 under MCA.

- LLP has perpetual succession which means leaving of partner from the firm will not affect the LLP firm. The firm will remain carry on it’s business.

- LLP is a body corporate and it has separate legal entity from its partners and have assets and liabilities that are separate from that of the partners Thus, an LLP is capable, in its own name, of acquiring, owning, holding, disposing of property, whether movable, immovable, tangible or intangible.

- Name of LLP can be changed .

- In an LLP there is no maximum limit on number of partners but LLP must have at least two individuals as Designated Partners. At least one of the Designated Partners must be resident in India (stays in India for at least 182 days during the preceding financial year) irrespective of their citizenship.

- In case number of Partners reduces below 2, the sole Partner will have the right to search a new Partner to fill the position without dissolution of the LLP.

- LLP have an easy and quick closure as compared to Company.

- In LLP there can be adding of partner or removal of partner.

Registration Procedure of Limited Liability Partnership

| Step I Basic check before Incorporation | • Identify designated partners

• Acquire Digital Signature (class 2) of the proposed designated partner (Atleast 1 DSC is required for Signing the Application) • Designated partner if does not hold DIN then will be allotted through Filing form only and no separate application is required. |

|---|---|

| Step II Approval of Name | • Check availability of name and get approval in RUN Form for LLP. |

| Step III Filing of Incorporation documents | • Apply for incorporation of LLP in Filling form "Form for Incorporation of Limited Liability Partnership" • Detailed description of all the partners and designated partner and subscriber sheet and attachment as required described below in detail. • Once the Form Filing is completed in all respect ,then it is to be digitally signed by designated partner and also to be certified by Advocate/CA/CS/Cost Accountants in practice. • The form after this need to be uploaded on MCA portal with the prescribed fees. |

| Step IV Certification of Registration | • Registrar after satisfying himself about completeness in documents and various compliances, issue certificate of incorporation. • In case of any discrepancies found in the form, then it comes in resubmission and need to be uploaded again with satisfying the remarks by MCA. |

| Step V Post incorporation compliance | • within 30 days of the incorporation, need to file Form 3 — LLP Agreement with the signed and stamped, notarized LLP Agreement. |

Documents Required for Limited Liability Partnership

- PAN Card and Adhar card (Mandatorily Required) of the Partners/Designated Partner

- Address Proof of the Partners/ Designated Partners (Voter id/ Driving License/ passport-anyone)

- Electricity Bill of the proposed Registered Office of the LLP (In case of owned)

- No-Objection Certificate from the Landlord, electricity bill and Rental Agreement Copy between the LLP and the Landlord (In case of Rented Office)

- Subscriber Sheet

- Consent of designated partner

- DSC of designated partner

E-Forms for Limited Liability Partnership

- LLP-RUN Form

- Fillip Form

- Form-3

Requirements for Limited Liability Partnership

- Minimum 2 Partners.

- Minimum 2 Designated Partners.

- At least 1 of the designated partners shall be an Indian Resident.

- If a body corporate is a partner, it has to nominate a natural person as its nominee

- No Minimum Capital Requirement.

- DPIN (Designated Partner Identification Number) for all the Partners.

- DSC (Digital Signature Certificate) for one of the Designated Partner.

Attachment To E-Form for Limited Liability Partnership

- Subscriber Sheet dully signed by all the partners

- Aadhar Card and Pan card of all the partners other than designated partners self-attested

- Designated Partner KYC Documents to be separately attached individually.

- Consent to act as designated Partner

- Registered office Address Proof as detailed above

- Companies in which Designated Partner is interested

Limited Liability Partnership Registration Fees

• Filing Form Fees as detailed below

| S.No. | Contribution Value in INR | Fee Payable in INR |

|---|---|---|

| 1. | Up to 1, 00, 000 | 500/- |

| 2. | More than 1,00,000 up to 5,00,000 | 2,000/- |

| 3. | More than 5,00,000 up to 10,00,000 | 4,000/- |

| 4. | More than 10,00,000 | 5,000/- |

• Name Reservation Fees of Run Form – Rs. 200

• Form -3 Filling Fees – Rs.50

Consequences of Non Compliance in LLP

Form -3 is to be filled within 30 days from the date of Incorporation and if any delay in filling the form then additional fees is charged of Rs. 100 on per day basis.

Advantages of Limited Liability Partnership

- Minimum capital requirements in LLP: LLP can be registered with any amount of capital that is mutually decided by partners in their LLP agreement so there is no limitation by the act.

- Less Registration Cost : The cost of registering LLP is low as compared to cost of incorporating a private limited or a One person company or public limited company.

- No compulsory Audit : There is no compulsory audit for LLP as compared to all limited companies. This is a important benefit of LLP. A Limited Liability Partnership is required to get the audited only when it crosses the following threshold limits:-

1. The contributions of the LLP exceeds Rs. 25 Lakhs, or

2. The annual turnover of the LLP exceeds Rs. 40 Lakhs - Limited Liability protection: Under LLP, one partner is not responsible or liable for another partner's misconduct or negligence. In case of any adverse situation in LLP, only investment to start a business is lost, personal assets of the Partners are safe.

- Better recognition in market: Corporate Customers, Vendors and Govt. Agencies prefer to deal with LLP instead of proprietorship or normal partnerships firms. LLP is having good credibility & recognition in the market as it is registered form of business with the central government.

Tax Computation of LLP (ITR Filing of LLP)

- For income tax purpose, LLP is treated on a par with partnership firms. Thus, LLP is liable for payment of income tax and share of its partners in LLP is not liable to tax. Thus no dividend distribution tax is payable. Provision of ‘deemed dividend’ under income tax law, is not applicable to LLP.

- Section 40(b): Interest to partners, any payment of salary, bonus, commission or remuneration allowed as deduction.

- The LLP is liable to pay income tax @30% on its income. In case the total income exceeds INR 1 Crore, LLP is also liable to pay surcharge @12% on the income tax. However, the surcharge shall be subject to marginal relief (where income exceeds one crore rupees, the total amount payable as income-tax and surcharge shall not exceed total amount payable as income-tax on total income of one crore rupees by more than the amount of income that exceeds one crore rupees). Additionally, health and education cess of 4% is payable on the income tax plus surcharge.

- Applicability of the provisions of AMT to LLPs: Vide Finance Act, 2011, the provisions of AMT were made applicable to the LLP. Provisions of AMT are applicable only in the following cases –

• When an LLP has claimed deduction under section 80H to 80RRB (except section 80P).

1. If an LLP has claimed deduction under section 35AD.

2. When an LLP has claimed deduction under section 10AA. - Rate of AMT @ 18.50% (plus surcharge and cess as applicable) of the adjusted total income is leviable.

- Reporting requirements: If AMT provisions apply to LLP, then, the LLP is required to obtain a report in FORM 29C from the Chartered Accountant. The said report certifies that the calculation of adjusted total income and the AMT is as per the applicable provisions.

Limited Liabilty Partnership Compliance

- ROC Annual Filing of LLP.

- E-KYC of Partners.

- Change in LLP Agreement.

- Adding of Partner to LLP.

- Removal of Partner from LLP.

- Change in Registered Office.

- Change in Name of LLP.

- Closure of LLP.

- ITR Filing of LLP.

What is Limited Liability Partnership (LLP)?

LLP gives the benefits of Limited Liability Company and flexibility of a Partnership Firm. It is an incorporated partnership formed and registered under the Limited Liability Partnership Act, 2008. LLP is a separate legal entity which can continue its existence irrespective of changes in its partners.

What is the concept of separate legal entity?

A company being a legal person is entirely distinct from its members and is capable of enter into contracts, possess properties in its own name, sue and can be sued by others etc.

What are the compliances of LLP registration?

Step I Basic check before Incorporation:

• Identify designated partners

• Acquire Digital Signature (class 2) of the proposed designated partner (Atleast 1 DSC is required for Signing the Application)

• Designated partner if does not hold DIN then will be allotted through Filing form only and no separate application is required.

Step II Approval of Name:

• Check availability of name and get approval in RUN Form for LLP.

Step III Filing of Incorporation documents:

• Apply for incorporation of LLP in Filling form "Form for Incorporation of Limited Liability Partnership"

• Detailed description of all the partners and designated partner and subscriber sheet and attachment as required described below in detail.

• Once the Form Filing is completed in all respect, then it is to be digitally signed by designated partner and also to be certified by Advocate/CA/CS/Cost Accountants in practice.

• The form after this need to be uploaded on MCA portal with the prescribed fees.

Step IV Certification of Registration:

• Registrar after satisfying himself about completeness in documents and various compliances, issue certificate of incorporation.

• In case of any discrepancies found in the form, then it comes in resubmission and need to be uploaded again with satisfying the remarks by MCA.

What is the post incorporation compliance of LLP?

Within 30 days of the incorporation of LLP, it is required to file Form 3 — LLP Agreement with the signed, stamped and notarized LLP Agreement.

What is the consequence of non-filing of Form 3 for the LLP Agreement?

Form-3 is to be filled within 30 days from the date of Incorporation and if any delay in filling the form then additional fees is charged of Rs. 100 on per day basis.

What is DPIN (Designated Partnership Identification Number)?

DPIN means an identification number which the Central Government may allot to any individual, intending to de appointed as designated partner or to an existing designated partner of a LLP, for the purpose of his identification as such. It is issued under section 7 of Limited Liability Partnership act, 2008 and rules made thereunder. DPIN is a unique identification number and once obtained is valid for lifetime of designated partner.

What are Government fees for registration of LLP?

• Filing Form Fees as detailed below

| S.No. | Contribution Value in INR | Fee Payable in INR |

|---|---|---|

| 1. | Up to 1, 00, 000 | 500/- |

| 2. | More than 1,00,000 up to 5,00,000 | 2,000/- |

| 3. | More than 5,00,000 up to 10,00,000 | 4,000/- |

| 4. | More than 10,00,000 | 5,000/- |

• Name Reservation Fees of Run Form – Rs. 200

• Form-3 Filling Fees – Rs.50

What are the documents required for registration of Limited Liability Partnership?

• PAN Card and Aadhar card (Mandatorily Required) of the Partners/Designated Partner

• Address Proof of the Partners/ Designated Partners (Voter id/ Driving License/ passport-anyone)

• Electricity Bill of the proposed Registered Office of the LLP (In case of owned)

• No-Objection Certificate from the Landlord, electricity bill and Rental Agreement Copy between the LLP and the Landlord (In case of Rented Office)

• Subscriber Sheet

• Consent of designated partner

• DSC of designated partner

What is DSC (Digital Signature Certificate)?

A Digital Signature is the electronic signature duly issued by certifying authority that shows the authority of the person signing the same. It is an electronic equivalent of a written signature. Every user who required to sign an e-form for submission with MCA is required to obtain a Digital Signature Certificate.

What is the minimum requirement for Limited Liability Partnership?

- Minimum 2 Partners.

- Minimum 2 Designated Partners.

- At least 1 of the designated partners shall be an Indian Resident.

- If a body corporate is a partner, it has to nominate a natural person as its nominee

- No Minimum Capital Requirement.

- DPIN (Designated Partner Identification Number) for all the Partners.

- DSC (Digital Signature Certificate) for one of the Designated Partner.

What are the advantages of LLP?

- Minimum capital requirements in LLP: LLP can be registered with any amount of capital that is mutually decided by partners in their LLP agreement so there is no limitation by the act.

- Less Registration Cost : The cost of registering LLP is low as compared to cost of incorporating a private limited or a One person company or public limited company.

- No compulsory Audit : There is no compulsory audit for LLP as compared to all limited companies. This is a important benefit of LLP. A Limited Liability Partnership is required to get the audited only when it crosses the following threshold limits:-

1. The contributions of the LLP exceeds Rs. 25 Lakhs, or

2. The annual turnover of the LLP exceeds Rs. 40 Lakhs - Limited Liability protection: Under LLP, one partner is not responsible or liable for another partner's misconduct or negligence. In case of any adverse situation in LLP, only investment to start a business is lost, personal assets of the Partners are safe.

- Better recognition in market: Corporate Customers, Vendors and Govt. Agencies prefer to deal with LLP instead of proprietorship or normal partnerships firms. LLP is having good credibility & recognition in the market as it is registered form of business with the central government.

What is the concept of Limited Liability Protection?

Under LLP, one partner is not responsible or liable for another partner's misconduct or negligence. In case of any adverse situation in LLP, only investment to start a business is lost, personal assets of the Partners are safe.

What are Tax provisions for LLP?

- For income tax purpose, LLP is treated on a par with partnership firms. Thus, LLP is liable for payment of income tax and share of its partners in LLP is not liable to tax. Thus no dividend distribution tax is payable. Provision of ‘deemed dividend’ under income tax law, is not applicable to LLP.

- Section 40(b): Interest to partners, any payment of salary, bonus, commission or remuneration allowed as deduction.

- The LLP is liable to pay income tax @30% on its income. In case the total income exceeds INR 1 Crore, LLP is also liable to pay surcharge @12% on the income tax. However, the surcharge shall be subject to marginal relief (where income exceeds one crore rupees, the total amount payable as income-tax and surcharge shall not exceed total amount payable as income-tax on total income of one crore rupees by more than the amount of income that exceeds one crore rupees). Additionally, health and education cess of 4% is payable on the income tax plus surcharge.

- Applicability of the provisions of AMT to LLPs: Vide Finance Act, 2011, the provisions of AMT were made applicable to the LLP. Provisions of AMT are applicable only in the following cases –

• When an LLP has claimed deduction under section 80H to 80RRB (except section 80P).

1. If an LLP has claimed deduction under section 35AD.

2. When an LLP has claimed deduction under section 10AA. - Rate of AMT @ 18.50% (plus surcharge and cess as applicable) of the adjusted total income is leviable.

- Reporting requirements: If AMT provisions apply to LLP, then, the LLP is required to obtain a report in FORM 29C from the Chartered Accountant. The said report certifies that the calculation of adjusted total income and the AMT is as per the applicable provisions.

What are the compliance requirements of LLP?

- ROC Annual Filing of LLP.

- E-KYC of Partners.

- Change in LLP Agreement.

- Adding of Partner to LLP.

- Removal of Partner from LLP.

- Change in Registered Office.

- Change in Name of LLP.

- Closure of LLP.

- ITR Filing of LLP.

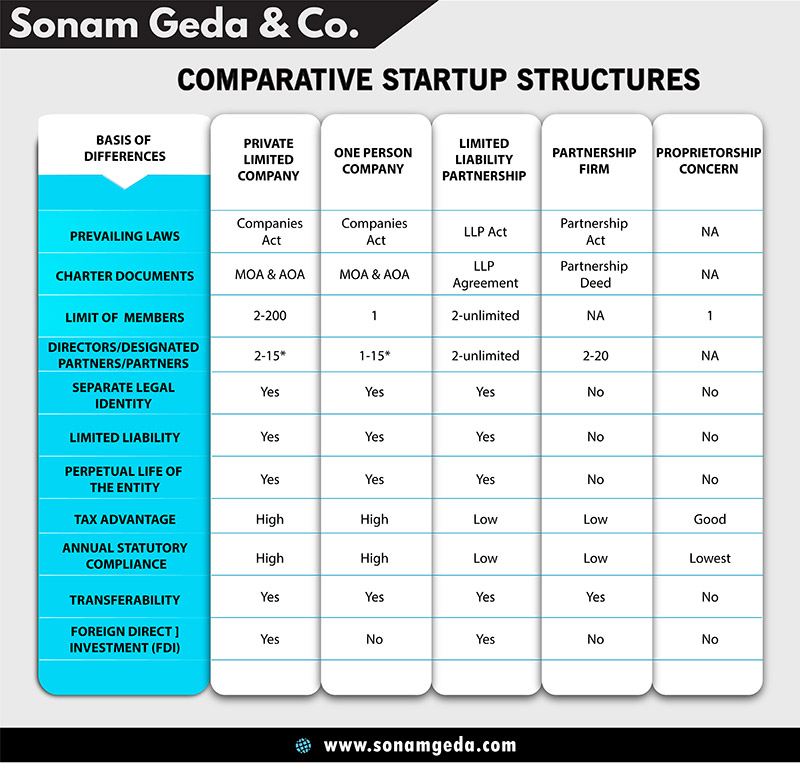

What is difference between LLP and different form of businesses?

We have prepared a detailed and easy to understand comparative table showing availability of features and advantages of one form of business to that of others. The same can be found at the end of this page.

Videos on LLP

To view video, click on image

Other Related Videos

To view video, click on image

Subscribe Our Newsletter

Get useful latest news & other important update on your email.