Non-Banking Financial Company

Sonam Geda & Company

Overview of NBFC (Non-Banking Financial Company)

A NBFC is a company registered under Companies Act, 2013 or Companies Act, 1956 which provide various financial and banking services such as providing loans and advances, acquiring stocks, equities, debts, etc. issued by government or any other local authority. NBFC provides various banking services but it does not hold banking license. These companies does not allowed to accept demand deposits from the public which differentiate it from banking companies. The NBFCs are regulated by the Ministry of Corporate Affairs and Reserve Bank of India as well.

Types of NBFC (Non-Banking Financial Company)

The NBFC can be categorised on the following basis:

- On the basis of activity it conducts.

- On the basis of deposits.

a) Deposit taking NBFC

b) Non-Deposit taking NBFC:

- Systemically important NBFC

- Other NBFC

Different types of NBFCs under above mentioned categories are as follows:-

1.Asset Finance Company (AFC): An AFC is a company which is engaged in the business of financing physical assets such as Automobiles, Industrial Machines, Tractors, etc.

2.Investment Company (IC): A Company which is carrying on the principal business of acquiring securities is known as Investment Company.

3.Loan Company (LC): It means a Company which is Financial Institution carrying on as its principal business of providing loans and advances for any activity but does not include AFC.

4.Infrastructure Finance Company (IFC): It is a Non-Banking Finance Company which fulfils following conditions:

a) Deploys at least 75% of its total assets in infrastructure loans

b) Having a minimum Net Owned Funds of ₹ 300 crore

c) Having a minimum credit rating of ‘A ‘or equivalent

d) Having CRAR of 15%

5.Infrastructure Debt Fund- Non-Banking Financial Company (IDF-NBFC): It is an NBFC which provide long term debt for Infrastructure Projects. IDF-NBFC shall be sponsored by IFC.

6.Mortgage Guarantee Company: It is a financial institution for which at least 90% of the business turnover is from mortgage guarantee business or at least 90% of gross income is from mortgage guarantee business and net owned fund is ₹ 100 crore.

7.Non-Banking Financial Company-Micro Finance Institution: It is a non-deposit taking NBFC having not less than 85% of its assets in the nature of qualifying assets which satisfy the criteria prescribed.

8.Systemically important Core Investment Companies: It is an NBFC which is engaged in the business of acquisition of shares and securities and satisfies the conditions prescribed.

9.Non-Banking Financial Company- Factors: It is a non-deposit taking NBFC carrying on the principal business of factoring. The financial assets in the factoring business should constitute at least 50% of its total assets and its income derived from factoring business should not be less than 50% of its gross income.

10.Non-Banking Financial Company-Non-operative Financial Holding Company: It is a setup of a new bank started by the promoters. It is a wholly-owned Non-Operative Financial Holding Company that holds the bank and other financial services regulated by RBI.

Requirements for Registration with RBI

A company incorporated under the Companies Act and desirous of commencing business of non-banking financial institution as defined under Section 45 I(a) of the RBI Act, 1934 should comply with the following:

- It should be a company registered under section 3 of Companies Act, 2013 or Companies Act, 1956.

- Minimum Net Owned Fund of Rs. 2 crore

- Minimum one full time director from the same background or a senior banker should be appointed

- Good CIBIL records of the company

Process of Registration of NBFC

- 1.Registration of a Company: A Company should first register under Companies Act, 2013 or Companies Act, 1956 with the main object of carrying on the business of NBFC. Only a registered company can apply for license of NBFC to Reserve Bank of India.

A Company should fulfil below mentioned minimum requirements:

• Minimum Net Owned Fund of Rs. 2 crore

• Minimum one full time director from the same background or a senior banker should be appointed

• Good CIBIL records of the company - 2. Open Bank Account of Company: After the registration of company Bank Account should be opened in the name of Company. In the Bank Account subscription amount should be deposited. But the Company cannot start business activities until license is issued by RBI.

- 3. Create a Fixed Deposit of Rs.2 crore: The Company should have the funds of Rs.2 crore and required to deposit that entire amount with the bank in the form of Fixed Deposit.

- 4. Then make an application on the RBI website along with the requisite documents for issue of license.

- 5. After submission of application on RBI website a CARN number will be generated.

- 6. A physical (hard) copy of the application along with the required documents should be submitted to the Regional Branch office of the RBI.

- 7. After the proper scrutiny of application, the license will be issued to the Company.

Documents Required for NBFC Registration

- Certified copy of the Certificate of Incorporation of the Company.

- Certified copy of MoA and AoA.

- Copy of PAN of the Company.

- List of Directors with attached signature of each Director.

- Credit report of Directors of the Company.

- Certificate from Statutory Auditor specifying owned funds of company as on Application date.

- Copy of Fixed Deposit receipt and Bankers Certificate of no lien indicating balances in support of Net Owned Fund.

- Copy of Board Resolution certifying that the company has not carrying on or stopped from carrying on NBFC activities.

- All information about the management of the company.

- Certificate from Statutory Auditor stating that the company is not holding deposits from public.

- Self-Certified copy of Bank Statement and Income Tax Return.

- Audited Accounts of the Company for last three consecutive years, (applicable in case company already in existence).

- Documents with respect to the location of the company.

- Other relevant documents, if requested.

Guidelines for NBFC

NBFC should adhere to the following guideline:

- A NBFC cannot accept deposits payable on demand.

- Duration of Public Deposit should not less than 12 months and should not exceed 60 months.

- The rate of interest charged by the company should not be more than the limit prescribed by the RBI.

- The company should submit the annual audited Balance Sheet.

- It should furnish the quarterly return on the Liquid Assets of the company.

- The RBI will not guarantee any repayment of amount by NBFC.

- Company should maintain atleast 15% of Public Deposits in Liquid Assets.

- The company should file Return on Deposits on deposits taken by it, in form NBS-1 every year.

- The company should take Credit Rating within every 6 months and submit the same with RBI.

Advantages of NBFC

- Evaluation of Borrower’s credibility: Before providing any loan NBFCs check the credibility of borrower or customer through credit score and business history of borrower. This makes recovery of loan more reliable.

- Easy Availability of Credit: NBFCs offer loans to customers on easy terms and conditions with fewer formalities. This makes it suitable for small borrowers.

- Unsecured Loans: NBFCs also provide unsecured loans to costumers. This facilitate borrower to take loan without mortgaging any assets or property.

- Enhances Standard of Living: Loans provided by NBFCs and growth of industrialisation increases the purchasing power of the individuals, which ultimately contributes in enhancing the standard of living.

- Provide Small Credit/Loans: Along with high value business loans needs NBFCs also entertain small credit needs of customer.

Disdvantages of NBFC

- NBFCs cannot accept Demand Deposits, since it lies within the dimension of commercial banks.

- Deposit Insurance Facility is not available for NBFC depositors.

- NBFCs cannot issue cheques drawn on itself, as it is not part of the payment and settlement system.

- All types of NBFCs cannot accept deposit from public.

- Regulatory mechanism for NBFCs is stringent.

Provision of Income Tax

Section 36(1)(viia) of the Income Tax Act provides for claim of deduction for the provision of Bad and Doubtful Debts for an amount not exceeding 5% of total income, computed before making deduction under clause (viia) of section 36(1) and Chapter VIA.

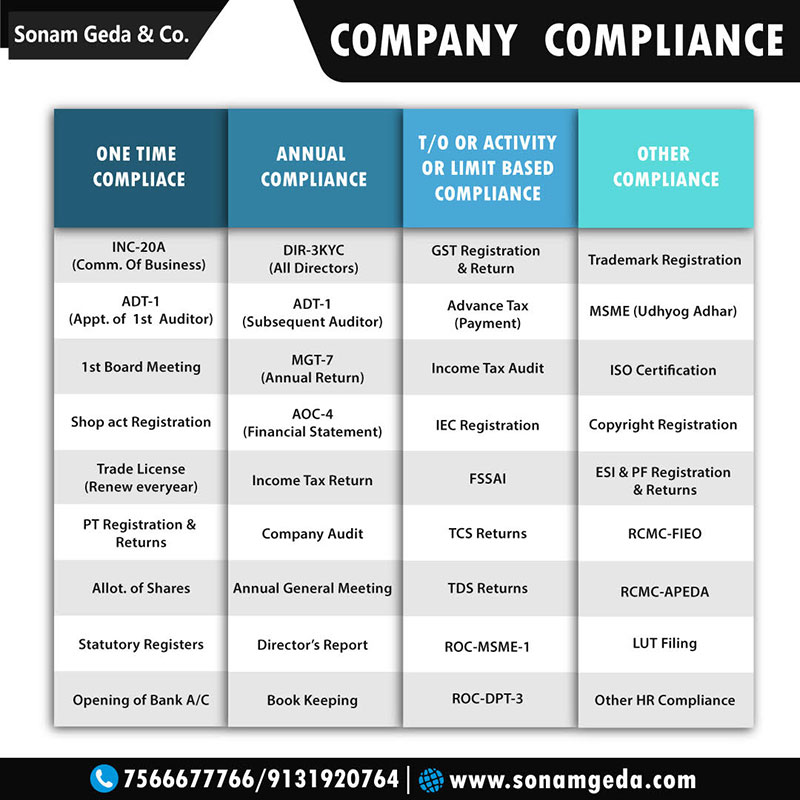

Compliances for NBFC

Every NBFC which has obtained license from RBI is required mandatorily comply with all annual compliances for NBFC. If it fails to comply it is liable for hefty penalties. Compliance requirement depends on the nature/type of NBFC.

What is NBFC (Non-Banking Financial Company)?

A NBFC is a company registered under Companies Act, 2013 or Companies Act, 1956 which provide various financial and banking services such as providing loans and advances, acquiring stocks, equities, debts, etc. issued by government or any other local authority. NBFC provides various banking services but it does not hold banking license. These companies does not allowed to accept demand deposits from the public which differentiate it from banking companies. The NBFCs are regulated by the Ministry of Corporate Affairs and Reserve Bank of India as well.

What are the types of NBFCs?

1.Asset Finance Company (AFC):

2.Investment Company (IC):

3.Loan Company (LC):

4.Infrastructure Finance Company (IFC):

5.Infrastructure Debt Fund- Non-Banking Financial Company (IDF-NBFC):

6.Mortgage Guarantee Company:

7.Non-Banking Financial Company-Micro Finance Institution:

8.Systemically important Core Investment Companies:

9.Non-Banking Financial Company- Factors:

10.Non-Banking Financial Company-Non-operative Financial Holding Company:

What are minimum requirements for registration of NBFC with RBI?

A company incorporated under the Companies Act and desirous of commencing business of non-banking financial institution as defined under Section 45 I(a) of the RBI Act, 1934 should comply with the following:

- It should be a company registered under section 3 of Companies Act, 2013 or Companies Act, 1956.

- Minimum Net Owned Fund of Rs. 2 crore

- Minimum one full time director from the same background or a senior banker should be appointed

- Good CIBIL records of the company

What is the process of incorporation of a NBFC?

- 1.Registration of a Company: A Company should first register under Companies Act, 2013 or Companies Act, 1956 with the main object of carrying on the business of NBFC. Only a registered company can apply for license of NBFC to Reserve Bank of India.

A Company should fulfil below mentioned minimum requirements:

• Minimum Net Owned Fund of Rs. 2 crore

• Minimum one full time director from the same background or a senior banker should be appointed

• Good CIBIL records of the company - 2. Open Bank Account of Company: After the registration of company Bank Account should be opened in the name of Company. In the Bank Account subscription amount should be deposited. But the Company cannot start business activities until license is issued by RBI.

- 3. Create a Fixed Deposit of Rs.2 crore: The Company should have the funds of Rs.2 crore and required to deposit that entire amount with the bank in the form of Fixed Deposit.

- 4. Then make an application on the RBI website along with the requisite documents for issue of license.

- 5. After submission of application on RBI website a CARN number will be generated.

- 6. A physical (hard) copy of the application along with the required documents should be submitted to the Regional Branch office of the RBI.

- 7. After the proper scrutiny of application, the license will be issued to the Company.

Which documents are required for registration of NBFC?

- Certified copy of the Certificate of Incorporation of the Company.

- Certified copy of MoA and AoA.

- Copy of PAN of the Company.

- List of Directors with attached signature of each Director.

- Credit report of Directors of the Company.

- Certificate from Statutory Auditor specifying owned funds of company as on Application date.

- Copy of Fixed Deposit receipt and Bankers Certificate of no lien indicating balances in support of Net Owned Fund.

- Copy of Board Resolution certifying that the company has not carrying on or stopped from carrying on NBFC activities.

- All information about the management of the company.

- Certificate from Statutory Auditor stating that the company is not holding deposits from public.

- Self-Certified copy of Bank Statement and Income Tax Return.

- Audited Accounts of the Company for last three consecutive years, (applicable in case company already in existence).

- Documents with respect to the location of the company.

- Other relevant documents, if requested.

What is the guideline for NBFCs?

NBFC should adhere to the following guideline:

- A NBFC cannot accept deposits payable on demand.

- Duration of Public Deposit should not less than 12 months and should not exceed 60 months.

- The rate of interest charged by the company should not be more than the limit prescribed by the RBI.

- The company should submit the annual audited Balance Sheet.

- It should furnish the quarterly return on the Liquid Assets of the company.

- The RBI will not guarantee any repayment of amount by NBFC.

- Company should maintain atleast 15% of Public Deposits in Liquid Assets.

- The company should file Return on Deposits on deposits taken by it, in form NBS-1 every year.

- The company should take Credit Rating within every 6 months and submit the same with RBI.

What are the advantages of NBFC?

- Evaluation of Borrower’s credibility: Before providing any loan NBFCs check the credibility of borrower or customer through credit score and business history of borrower. This makes recovery of loan more reliable.

- Easy Availability of Credit: NBFCs offer loans to customers on easy terms and conditions with fewer formalities. This makes it suitable for small borrowers.

- Unsecured Loans: NBFCs also provide unsecured loans to costumers. This facilitate borrower to take loan without mortgaging any assets or property.

- Enhances Standard of Living: Loans provided by NBFCs and growth of industrialisation increases the purchasing power of the individuals, which ultimately contributes in enhancing the standard of living.

- Provide Small Credit/Loans: Along with high value business loans needs NBFCs also entertain small credit needs of customer.

What are the disadvantages of NBFC?

- NBFCs cannot accept Demand Deposits, since it lies within the dimension of commercial banks.

- Deposit Insurance Facility is not available for NBFC depositors.

- NBFCs cannot issue cheques drawn on itself, as it is not part of the payment and settlement system.

- All types of NBFCs cannot accept deposit from public.

- Regulatory mechanism for NBFCs is stringent.

What is tax provision for NBFC?

Section 36(1)(viia) of the Income Tax Act provides for claim of deduction for the provision of Bad and Doubtful Debts for an amount not exceeding 5% of total income, computed before making deduction under clause (viia) of section 36(1) and Chapter VIA.

What are the compliances for NBFC?

Every NBFC which has obtained license from RBI is required mandatorily comply with all annual compliances for NBFC. If it fails to comply it is liable for hefty penalties. Compliance requirement depends on the nature/type of NBFC.

What is difference between NBFC and Bank?

Unlike banks NBFCs are not allowed to issue self-drawn cheques and demand drafts. These companies does not allowed to accept demand deposits from the public which differentiate it from banking companies.

Who is regulator of NBFC?

Non- Banking Financial Companies are regulated by the Ministry of Corporate Affairs and Reserve Bank of India as well.

Videos on NBFC Company

To view video, click on image

Other Related Videos

To view video, click on image

Subscribe Our Newsletter

Get useful latest news & other important update on your email.